The South African sugar industry is one of the world’s top producers of high-quality sugar. The industry has 21 926 registered sugarcane growers who produce 20 million tonnes of sugarcane per year, according to 2019/2020 figures (SASA, 2020). South Africa has 14 sugar mills in operation operated by 6 milling companies. Farming and processing sugarcane in South Africa occurs in the northeastern parts of the country, primarily in Kwa-Zulu Natal, with some farming and milling occurring in Mpumalanga.

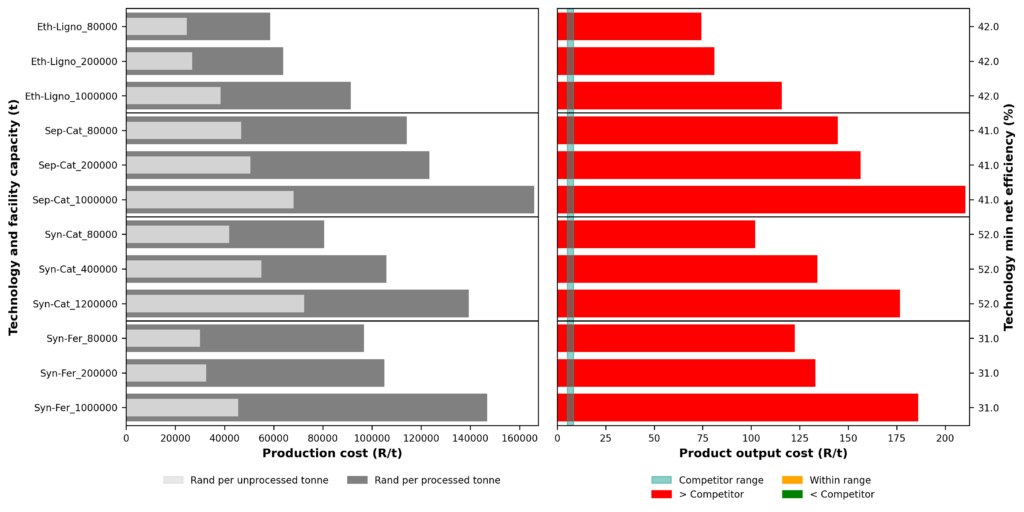

The sugar industry has been facing many challenges, such as increasing production costs and competing with cheap sugar imports. Additionally, the newly implemented government law on sugar tax has also led to a decrease in demand for sugar and a surplus in production. According to the South African Sugar Association (SASA) and South African Cane Growers Association (SACGA), the sugar industry experienced over a 30 percent decrease in the amount of sugar sold to the beverage sector since April 2018 (Sikuka, 2019). As a result, the sugar industry estimates that its revenue will drop by approximately R1.8 billion (SA Canegrowers, 2017). All these challenges are affecting the sugar industry’s return on sales.

The sugar industry has been exploring other manufacturing methods, such as diversification of the industry. Diversification of the sugar industry would transform sugar mills into bio-energy complexes that would produce ethanol and electricity in addition to sugar (Farzad et al., 2017). This plan of the sugar industry is in line with the South African government’s National Development Plan (NDP) (South African Government,2012), which seeks to grow the economy and create jobs by 2030. The plan aims to resolve the energy crisis, improve energy infrastructure and reduce carbon emissions by diversifying the energy mix. Internationally, countries such as Brazil, Thailand, and Australia have already diversified their sugar industries.

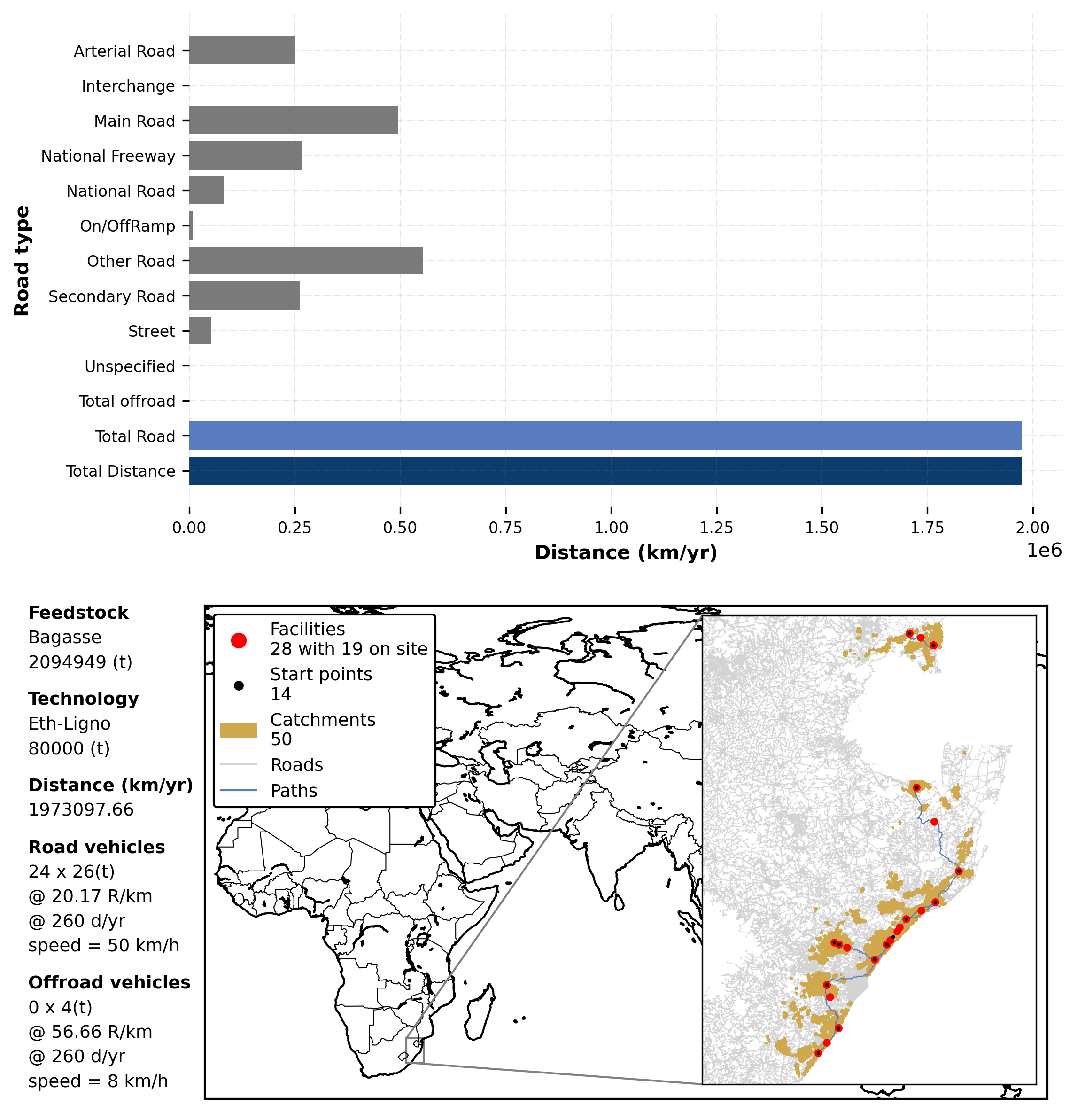

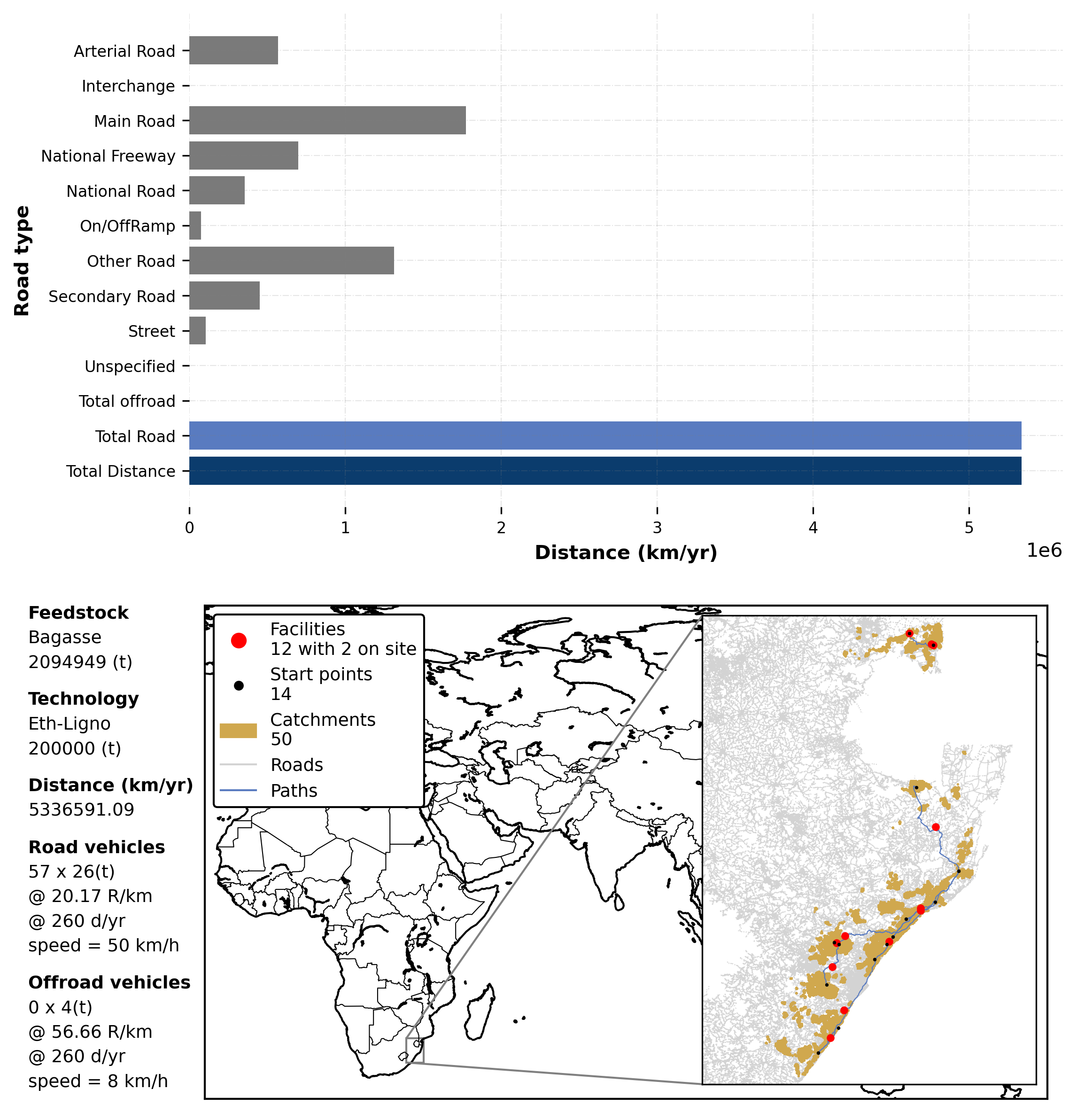

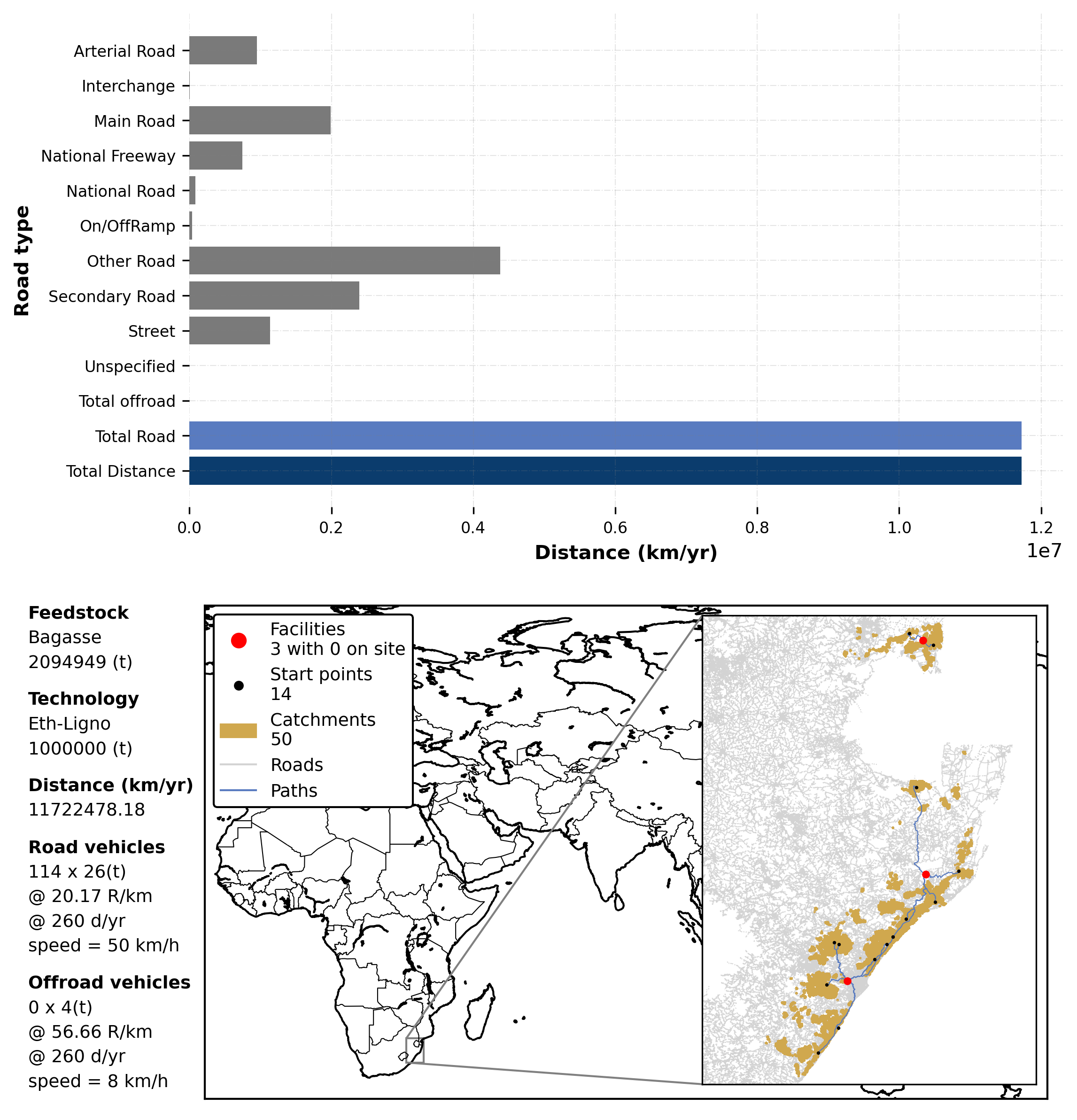

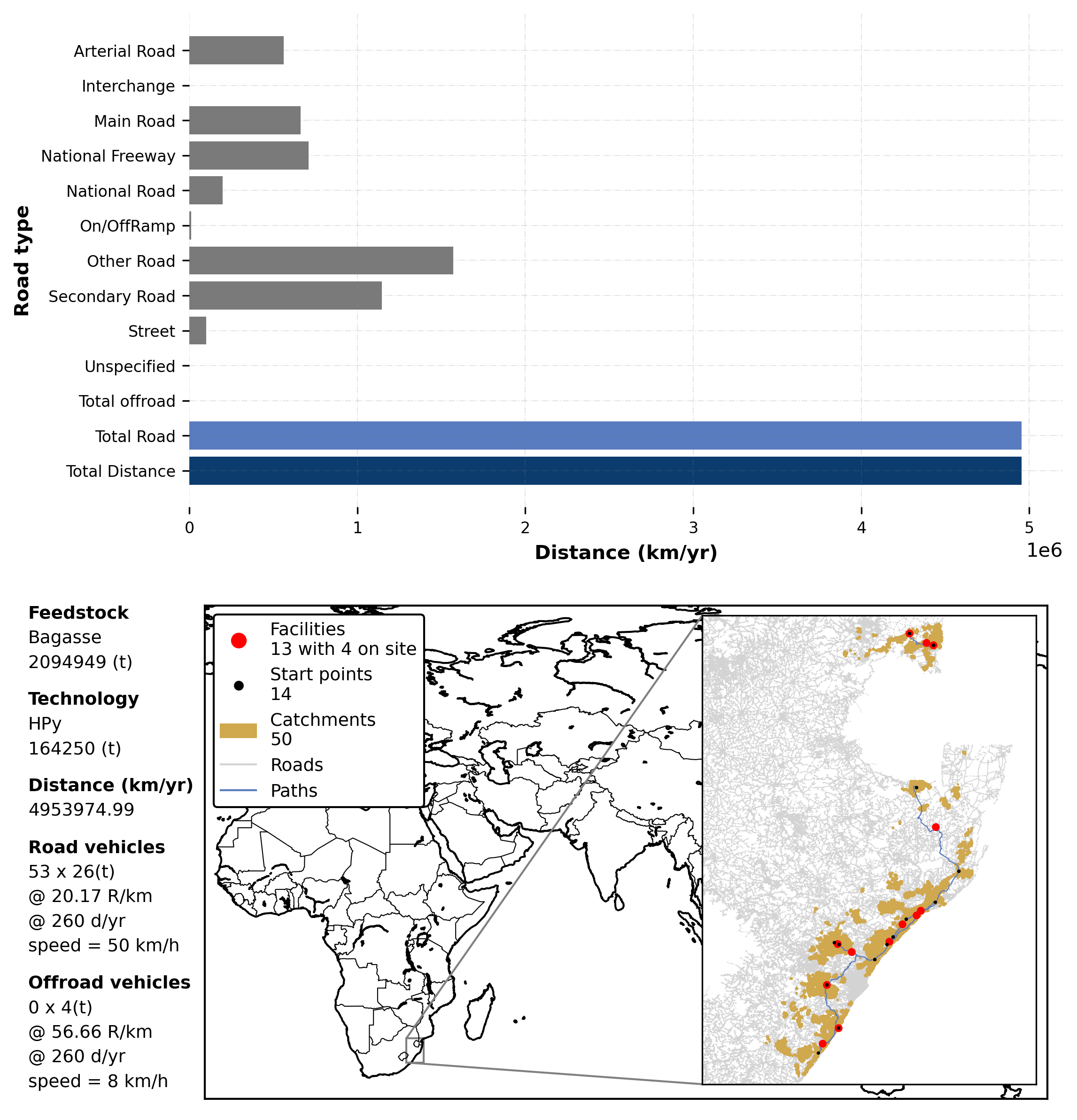

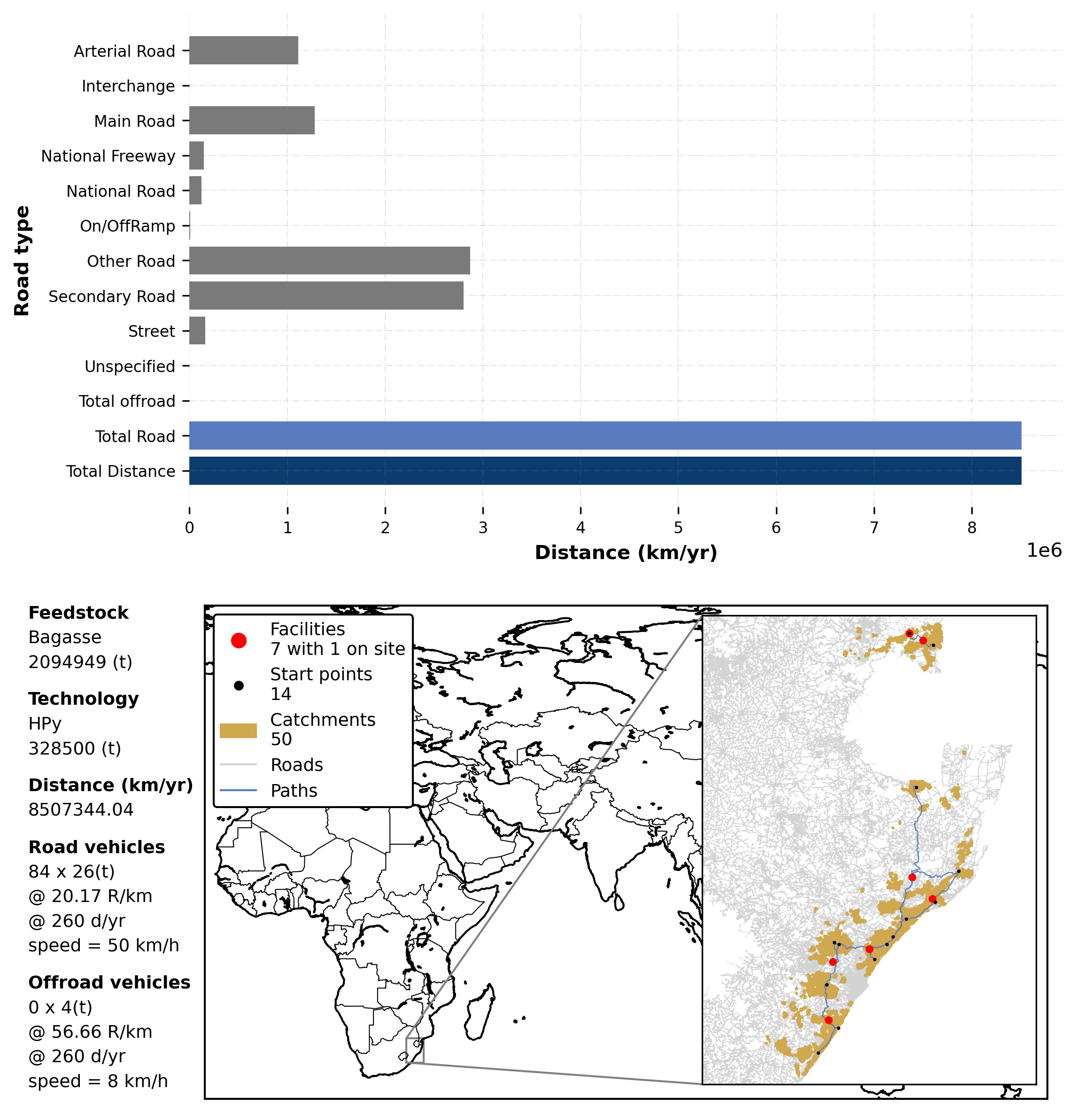

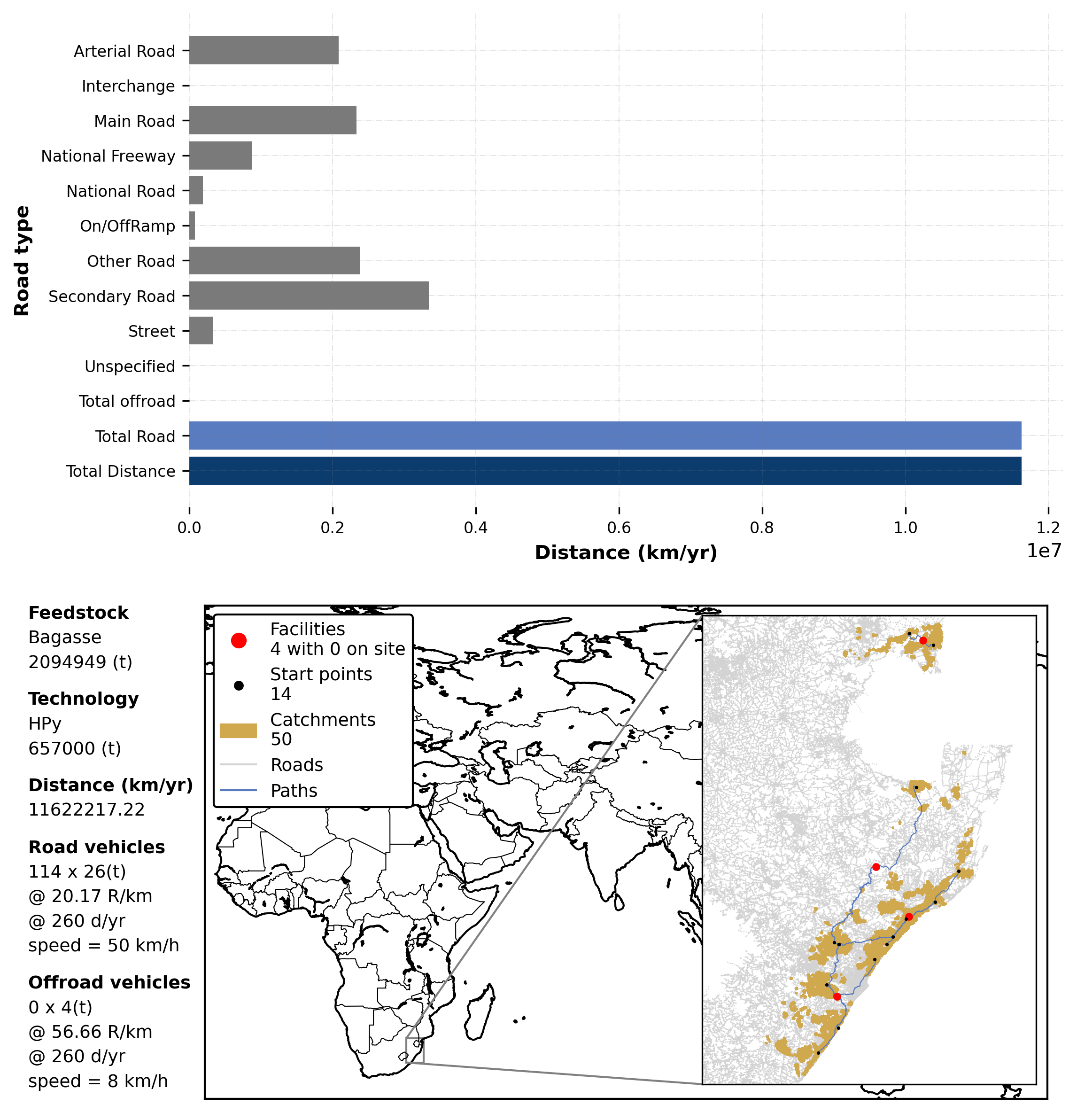

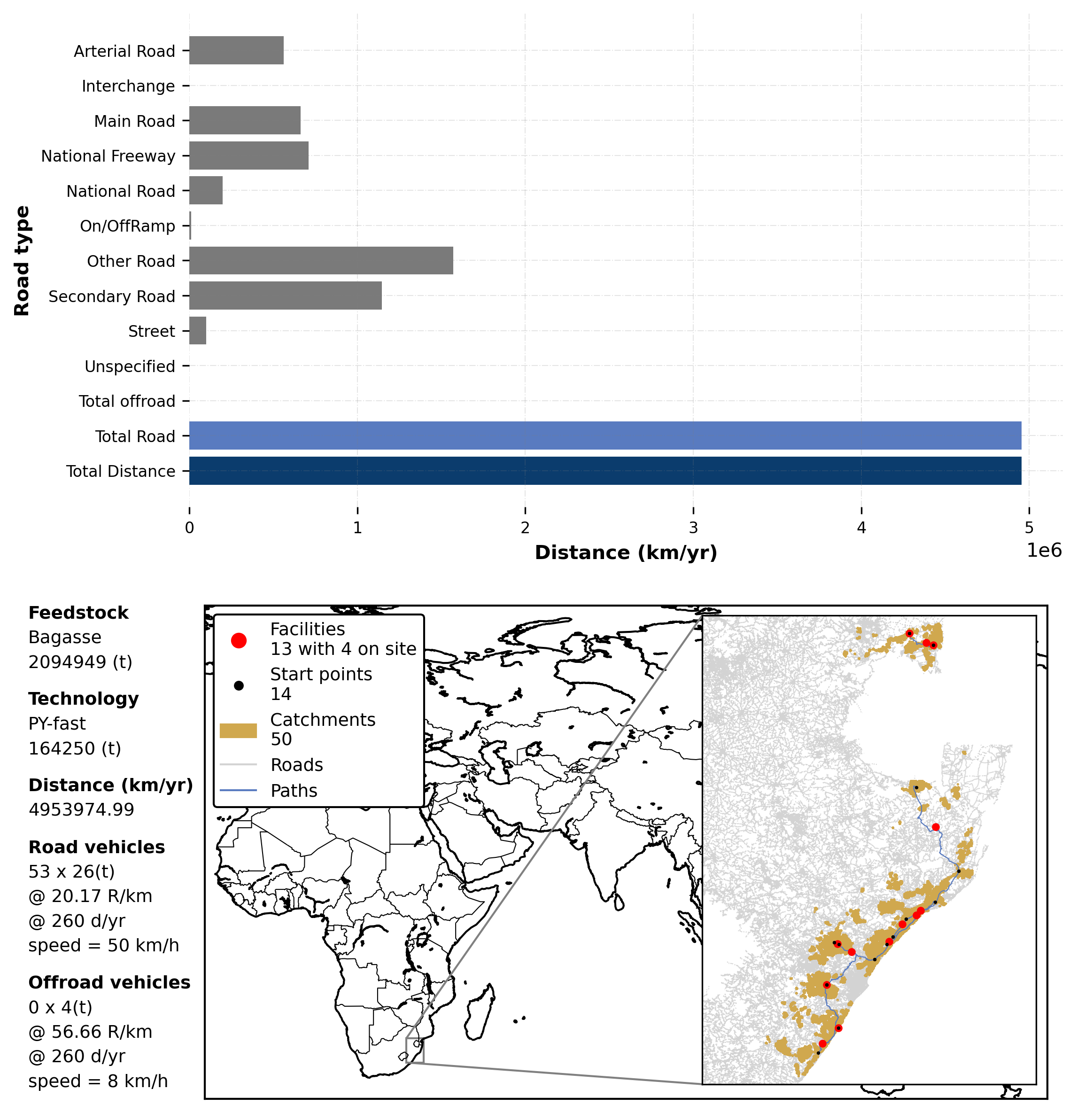

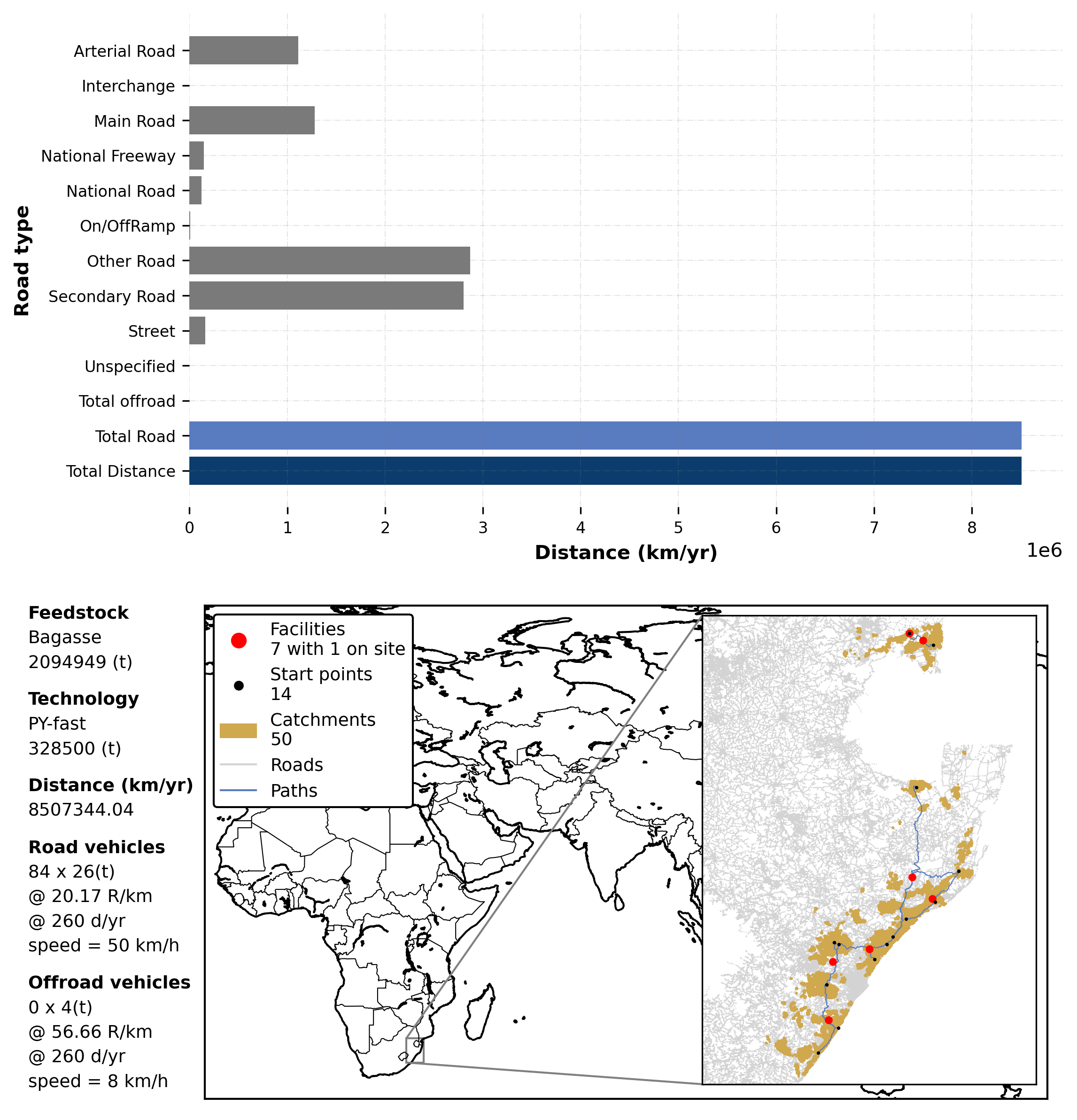

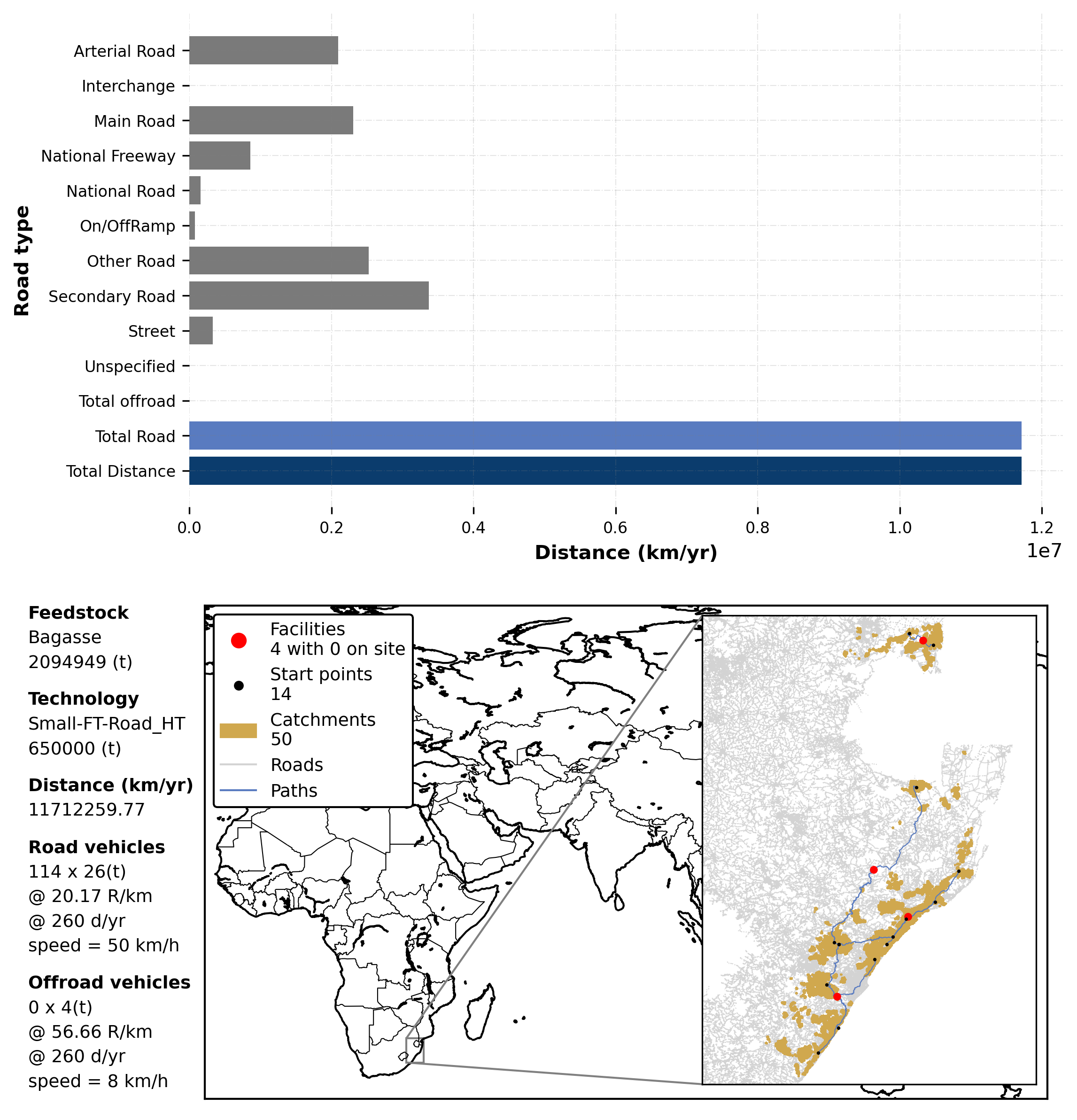

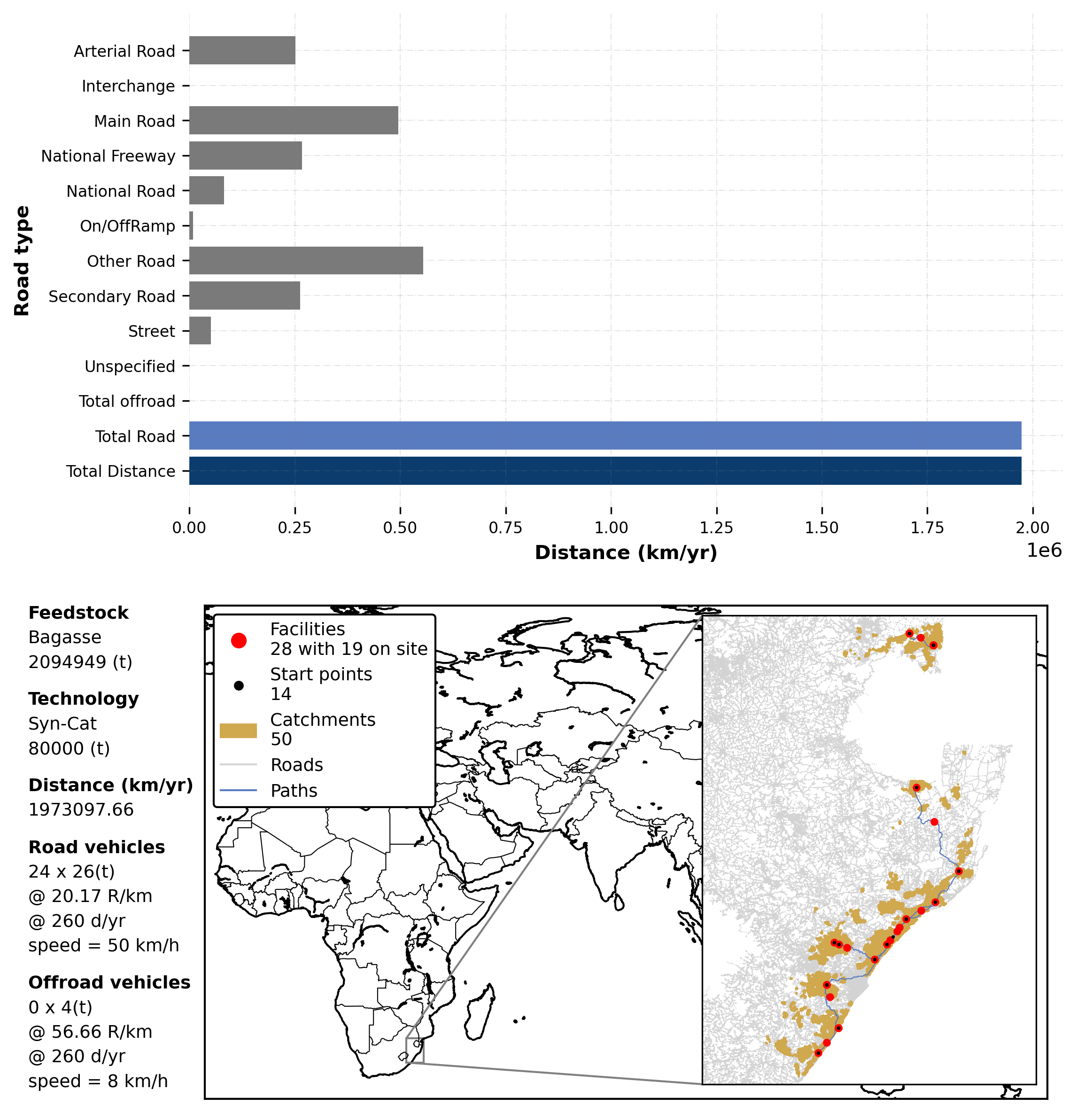

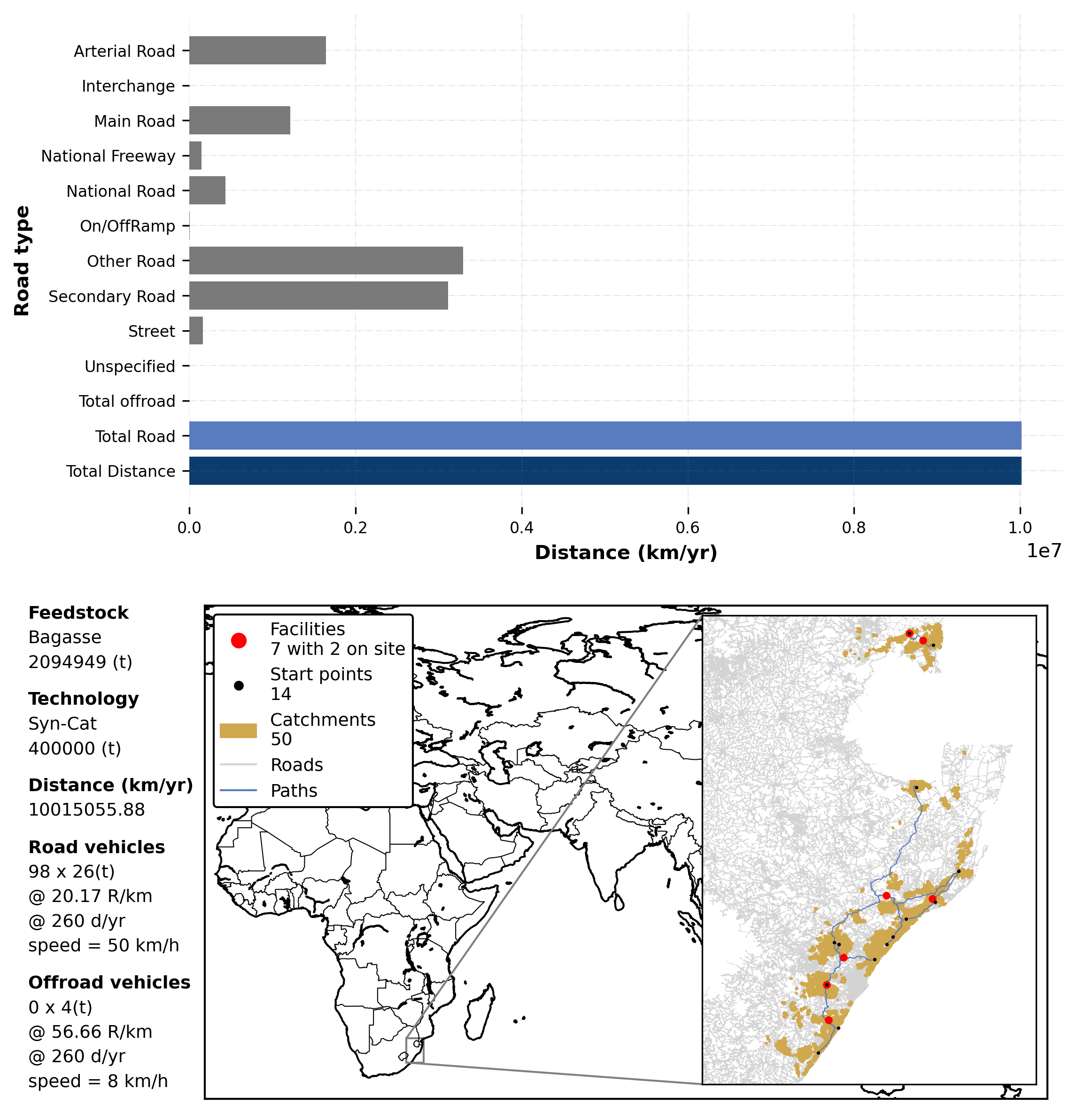

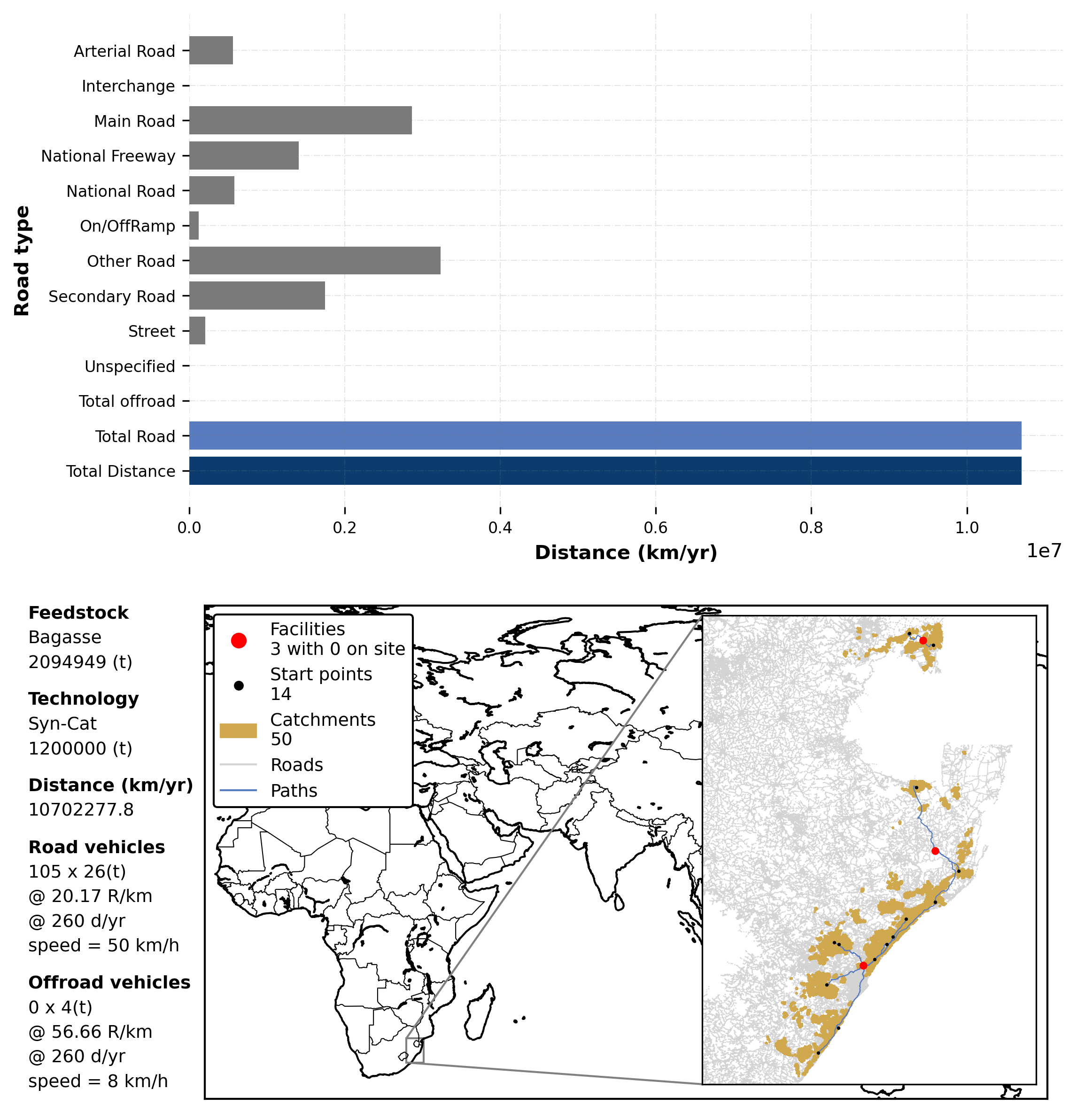

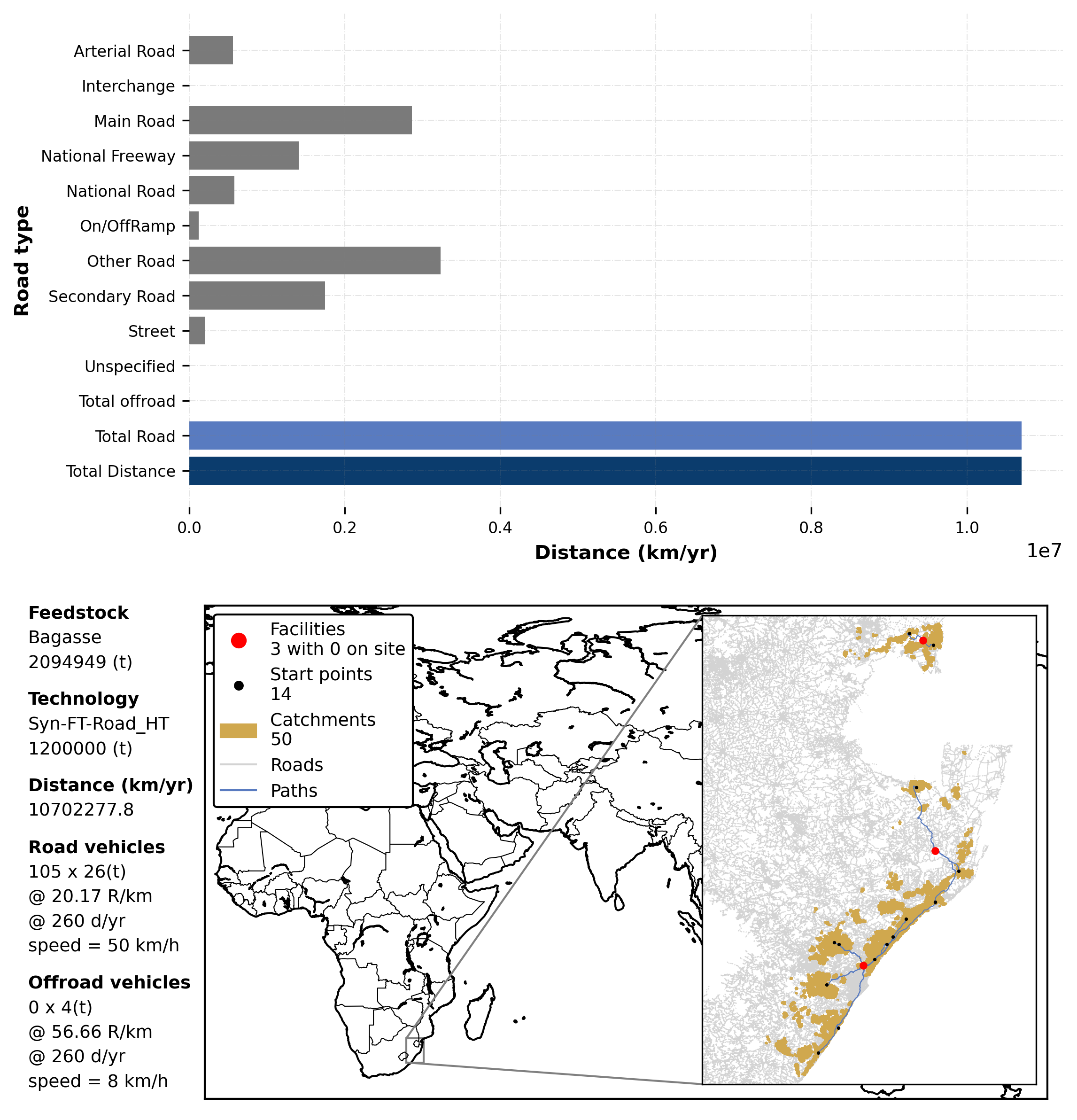

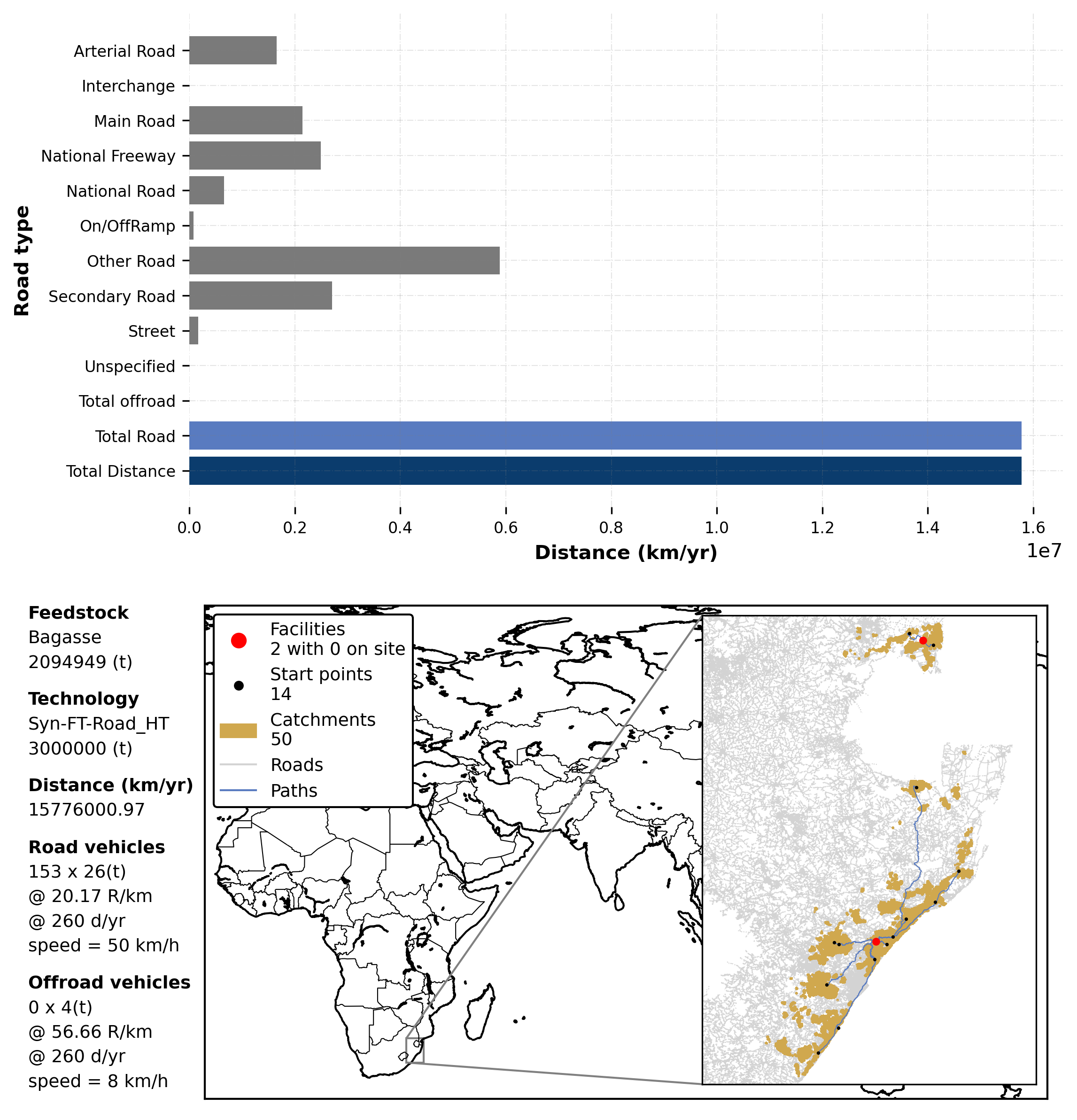

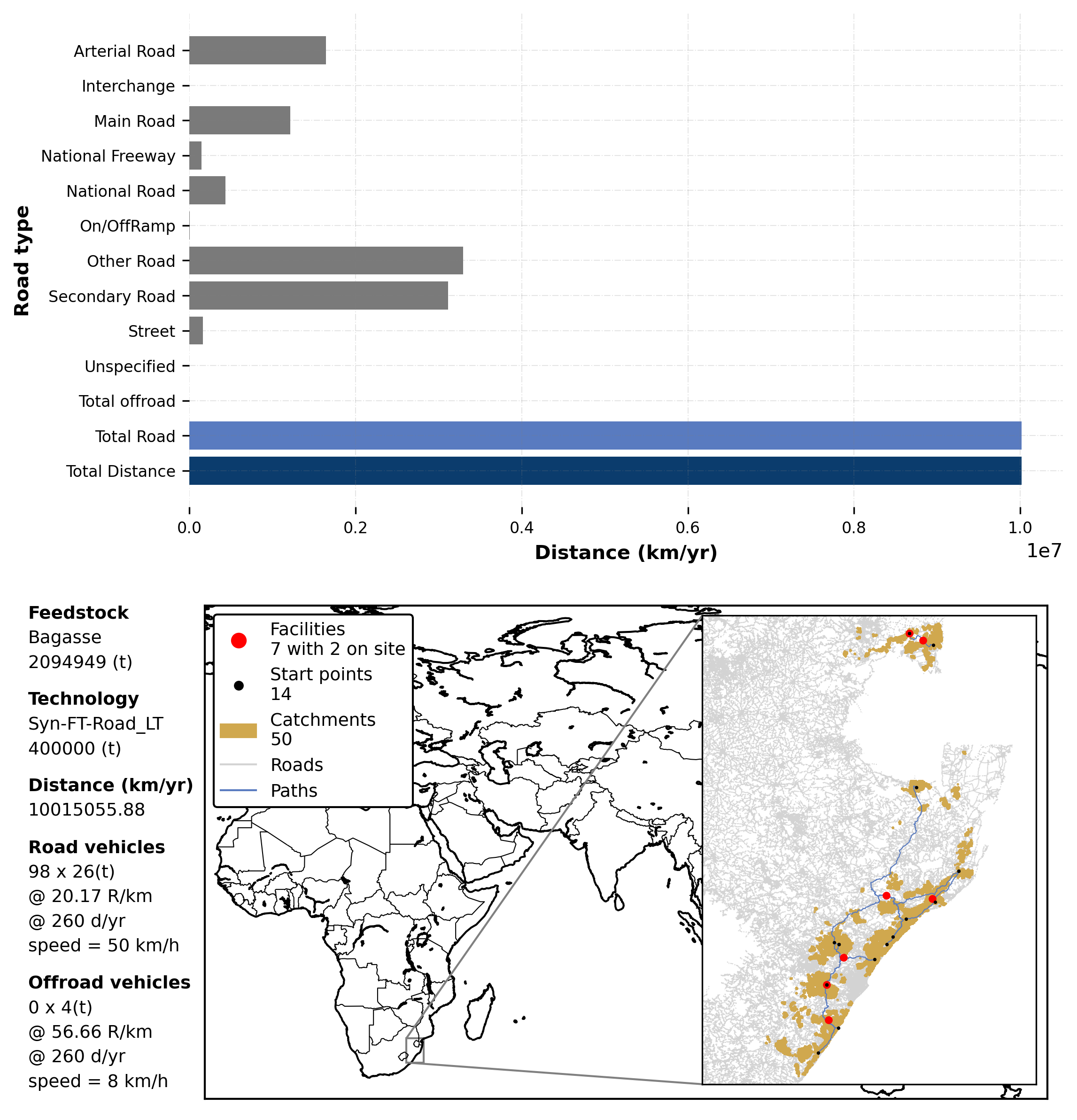

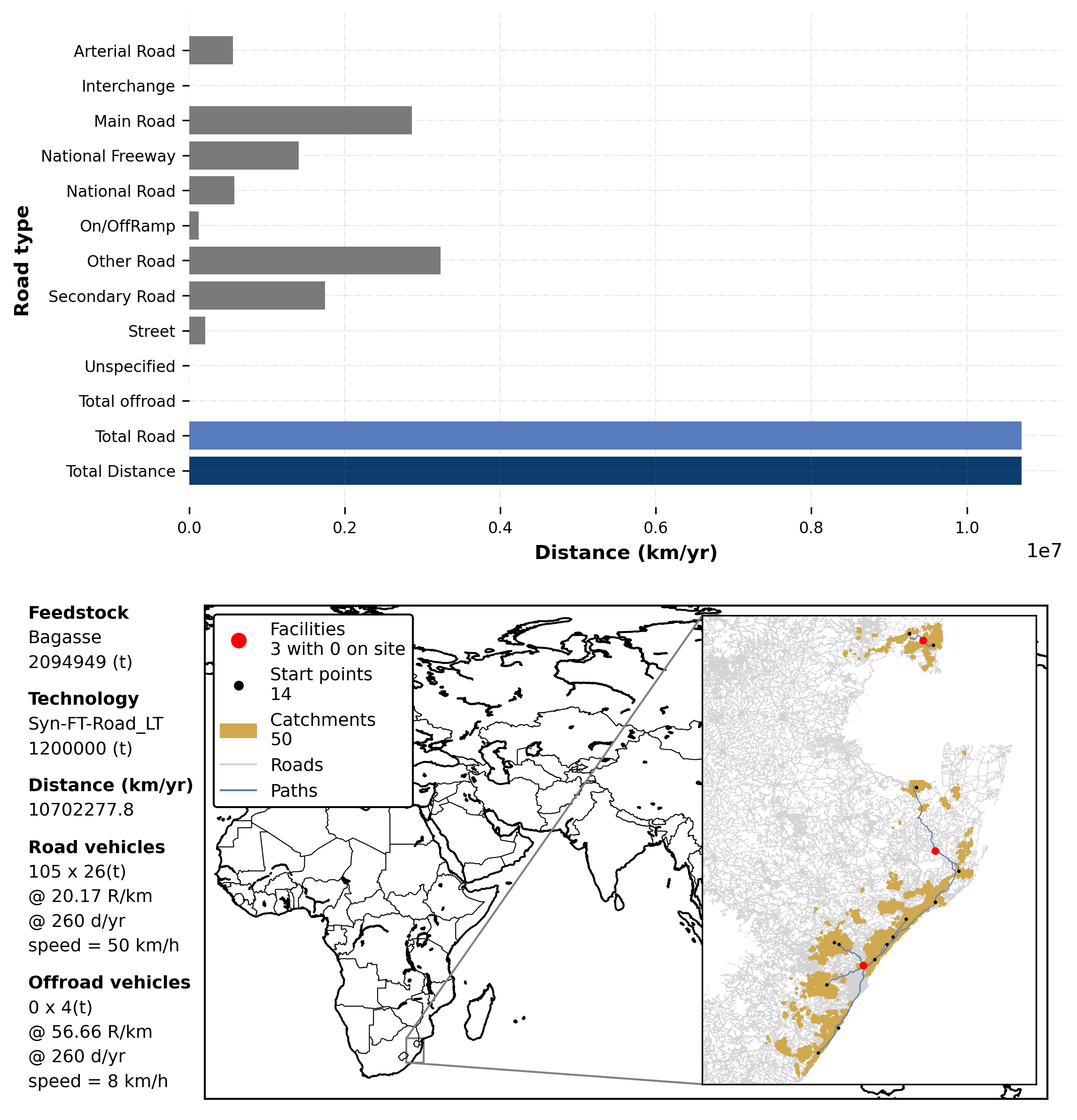

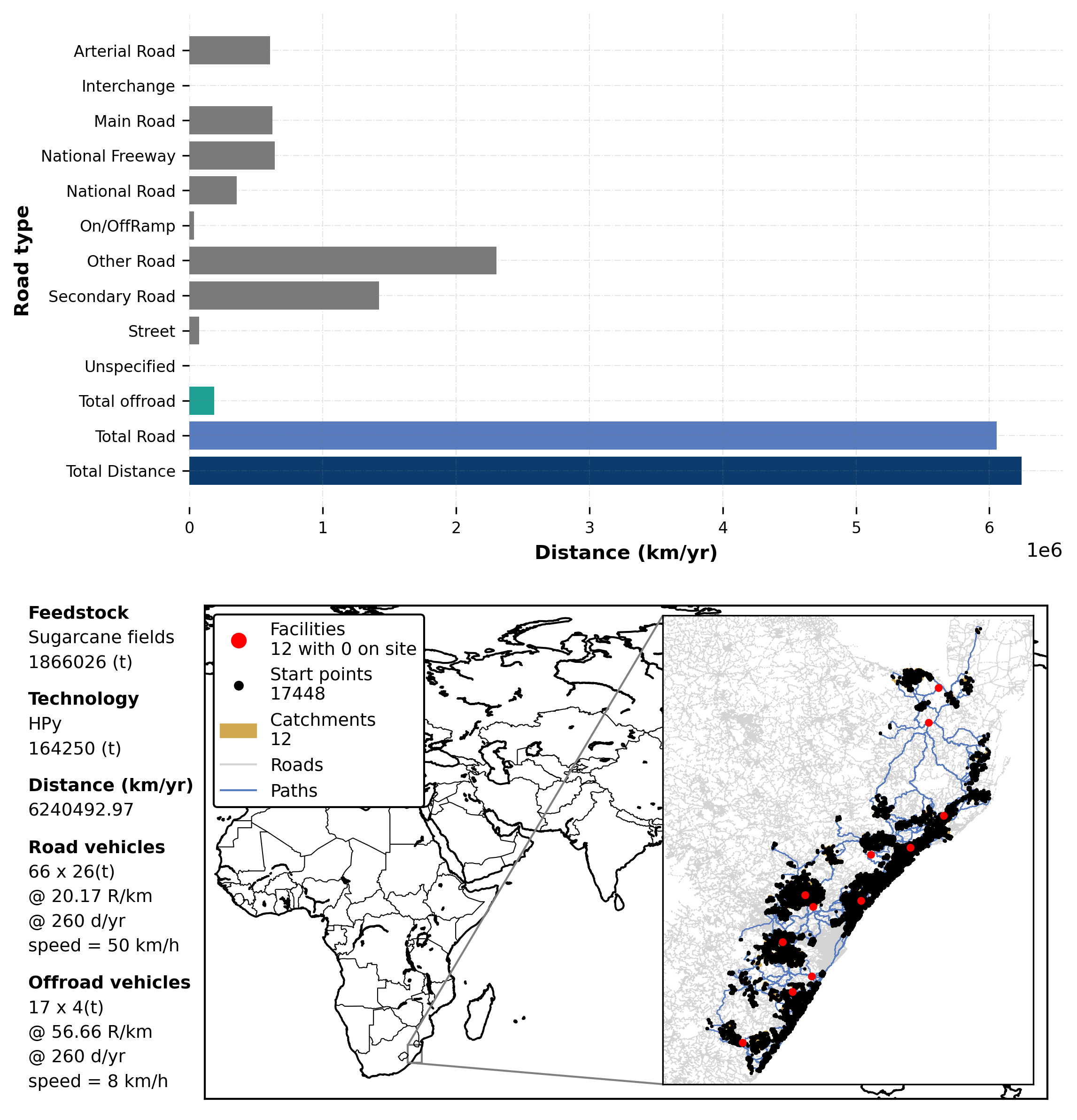

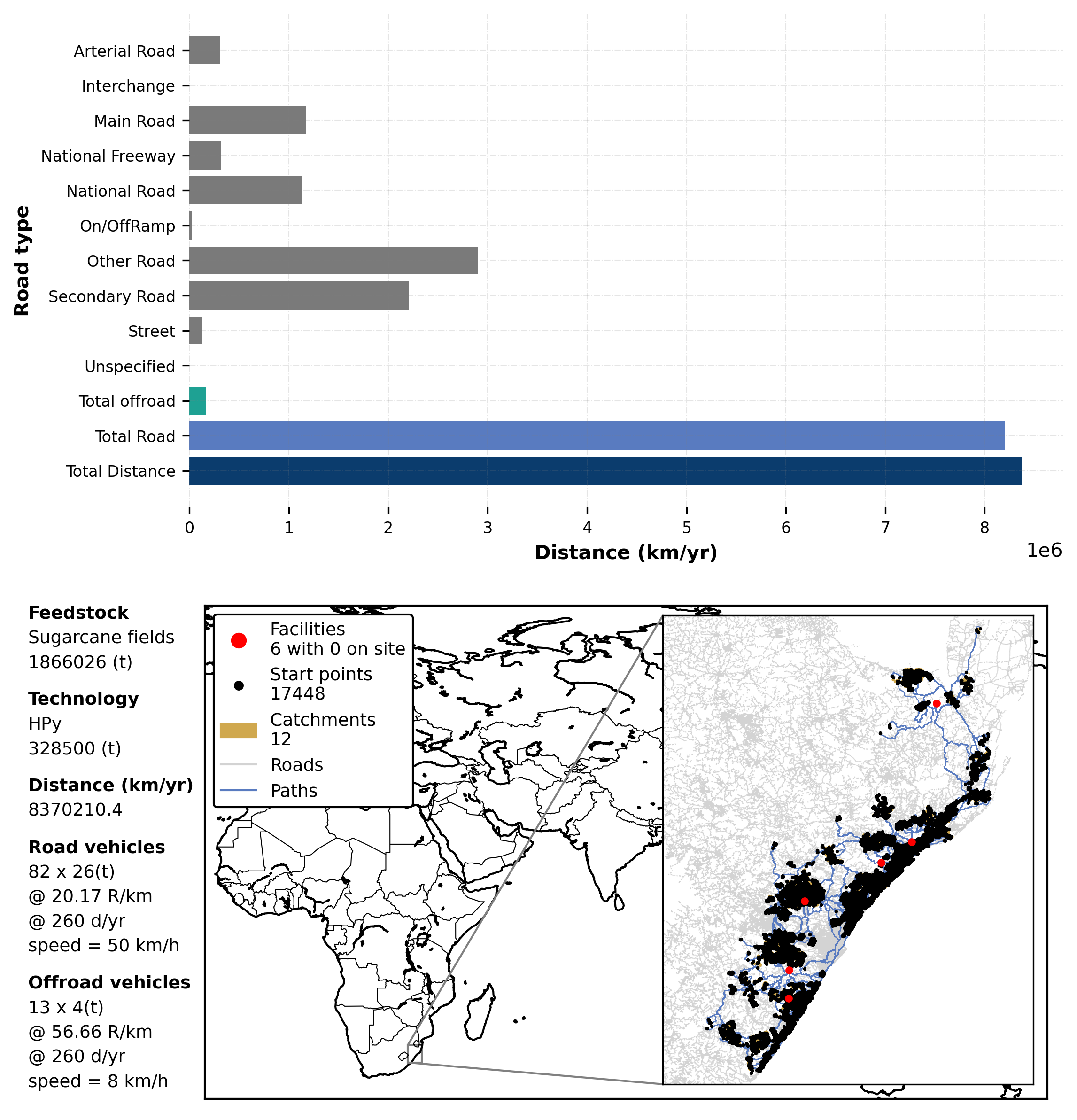

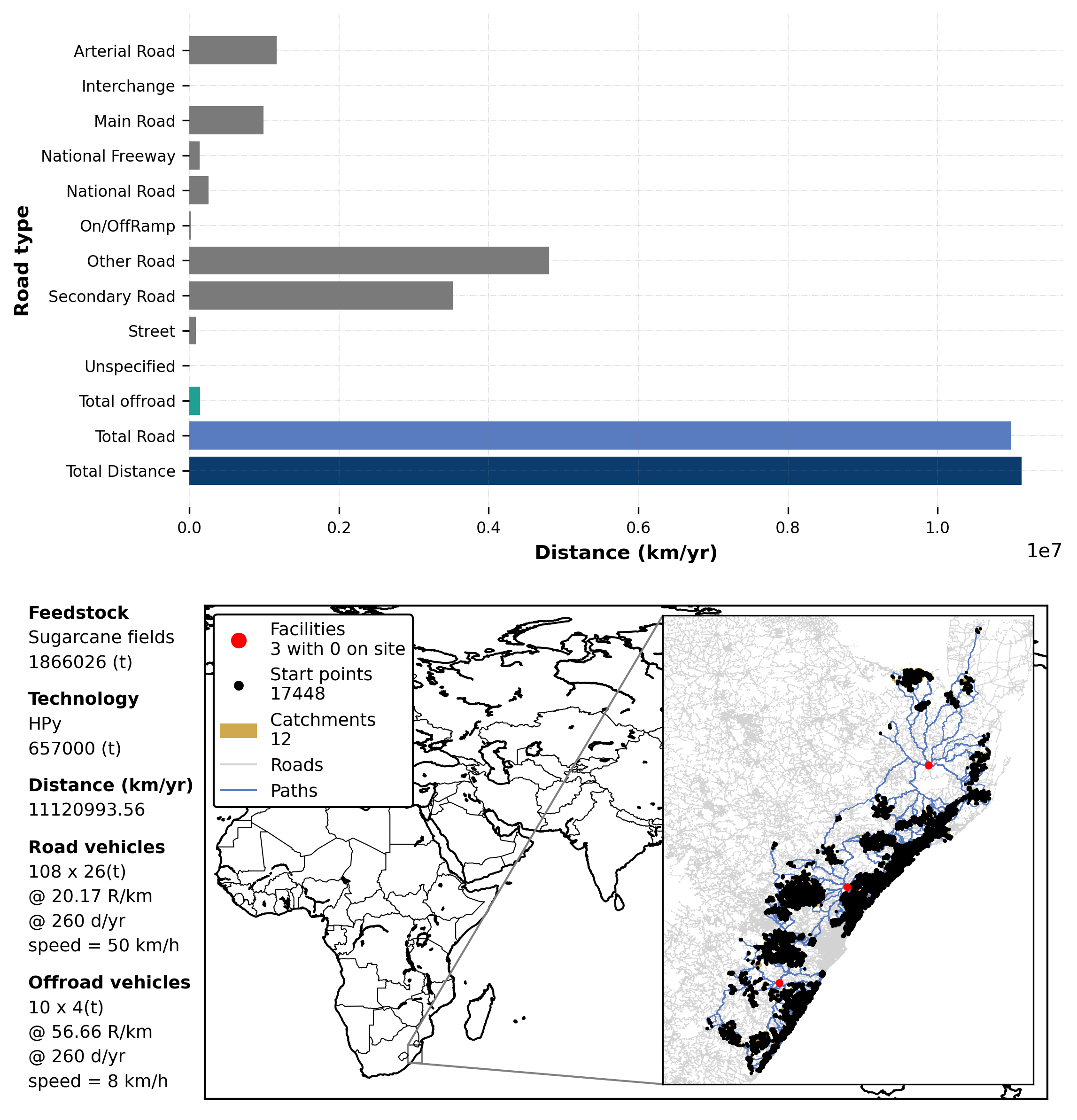

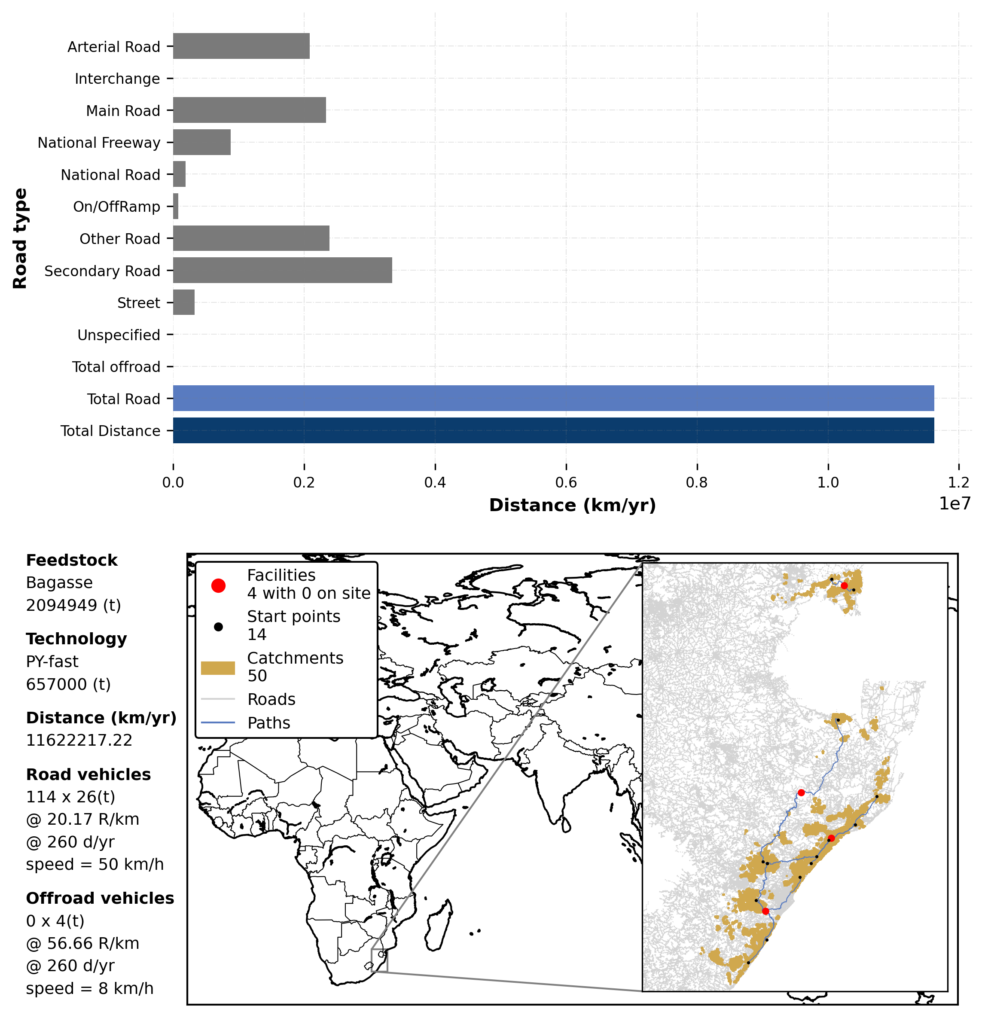

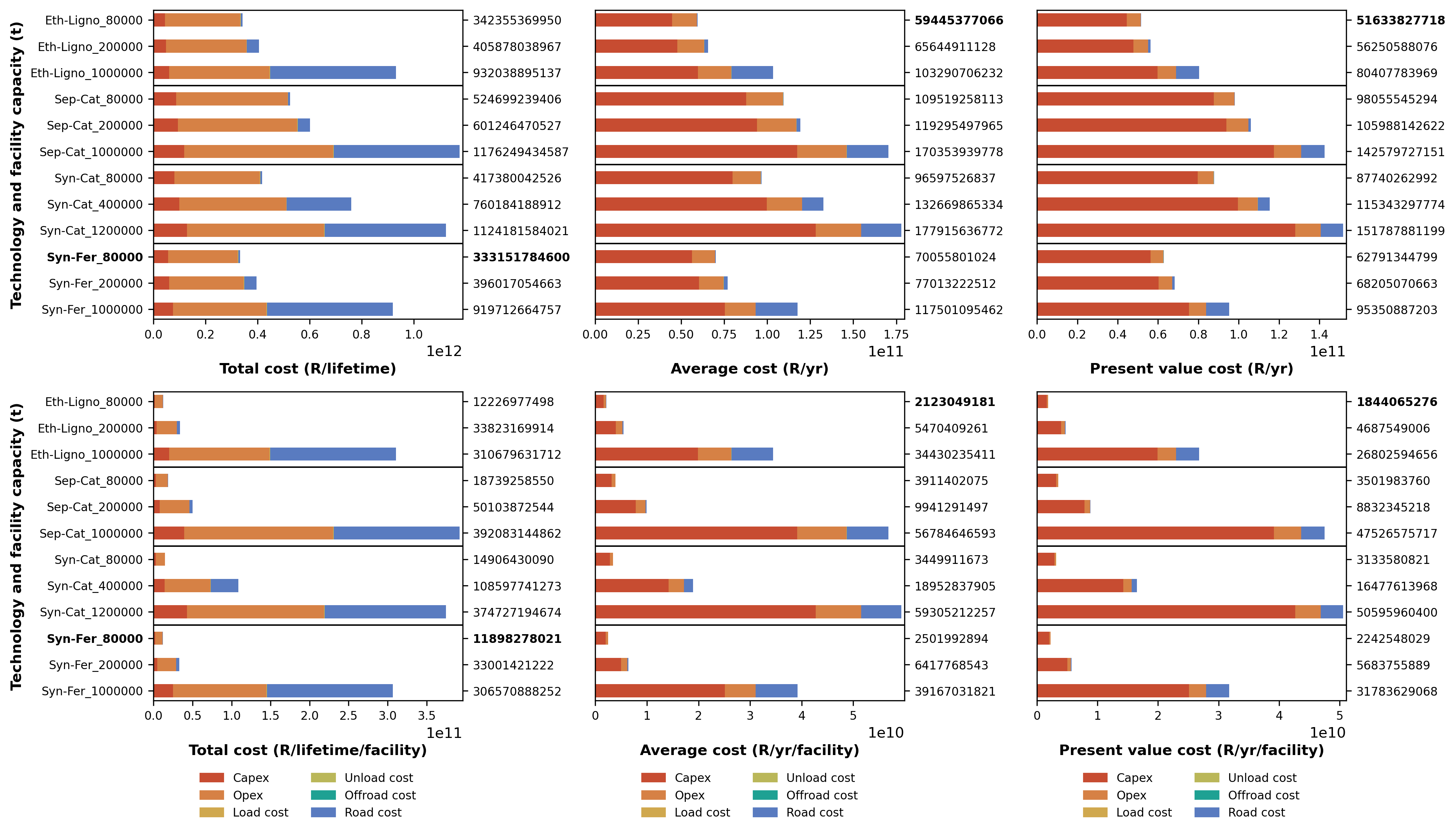

The sugarcane industry generates a large amount of lignocellulosic biomass derived from sugarcane, biomass consists of the residue that remains in the field after the sugarcane harvest, and the residue left after the milling process. The milling of sugarcane to extract the juice generates bagasse (the fibrous biomass remaining after stalks are crushed to extract the liquid), while field residue consists of stalk, mulch, and brown leaves. Lignocellulosic biomass can be used as feedstock to produce second-generation (2G) ethanol which can be used to replace or be mixed with petroleum fuels

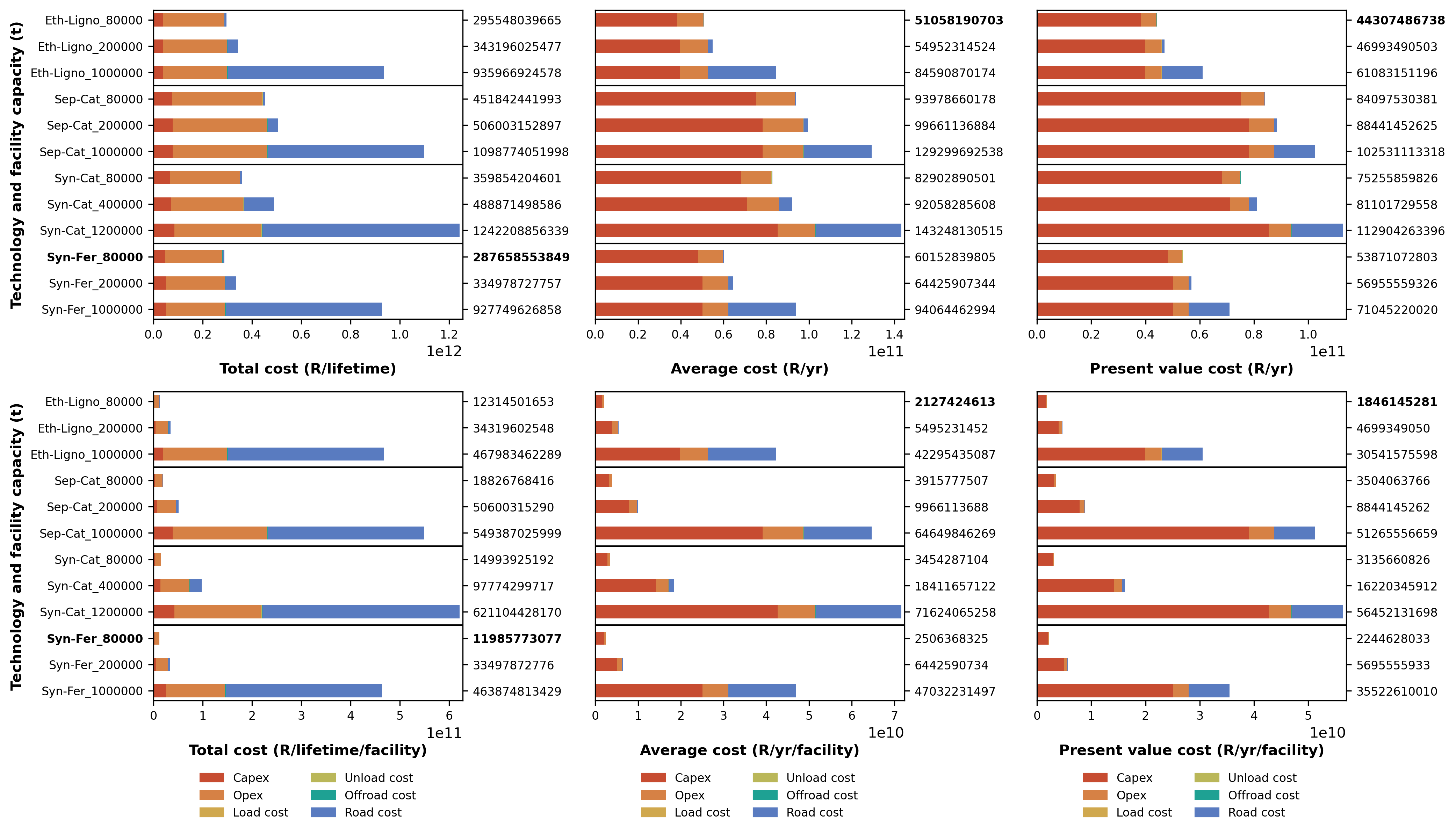

This case study will investigate the techno-economic feasibility of using sugarcane field residue or mill residue as feedstock to produce ethanol and transport fuels. The techno-economic feasibility analysis for the study assesses conventional technologies with an end product of ethanol, diesel, or gasoline.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()